By Peter Gratton

:max_bytes(150000):strip_icc():format(webp)/PGphotobestversion-c7f87d2cc1ef41459cf33551c7bd3530.jpg)

Peter Gratton, Ph.D., is a New Orleans-based editor and professor with over 20 years of experience in investing, economics, and public policy. Peter began covering markets at Multex (Reuters) and has expanded his coverage to include investments, ethics, public policy, and the health and travel industries.

Learn about our editorial policies

Published March 11, 2026

:max_bytes(150000):strip_icc():format(webp)/ptLxV-average-student-loan-balance-per-borrower-by-state--9ad532f6621141c3bbe22ca883f3be9c.png)

25 Highest Paid Occupations in the USClose

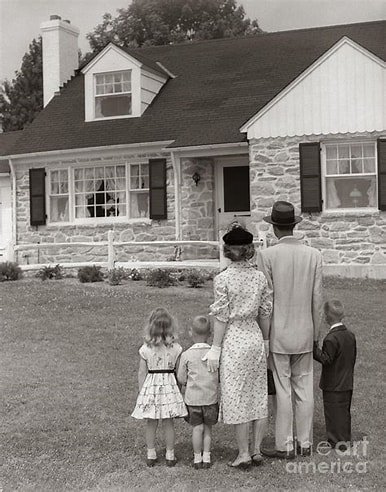

Key Takeaways

- Americans owe $1.66 trillion in student loan debt, but the average per-borrower balance varies dramatically by state.

- Even as total student debt has climbed, the average balance per borrower dropped in 47 states in 2025, a sign that millions of borrowers who paused payments earlier this decade have been making a dent as they resume payments.

- The average amount of student loan debt nationwide is $54,600.

The average student loan borrower in Washington, D.C., owes $126,500.1 In Wyoming, it’s $31,800.

That $94,700 gap reflects local demographics and job growth. But it’s also a sign of where advanced degrees are concentrated in America, as well as how the weight of that borrowing keeps millions from buying homes and building savings.

Where the Debt Is the Highest

After D.C., Georgia holds the highest average per-borrower balance in the country at $71,200. That figure makes sense in light of Atlanta’s density of historically Black colleges and universities compared with the rest of the South.1 Maryland ($68,300) and New Jersey ($65,400) follow, with Connecticut, Pennsylvania, and Delaware all above $63,000.

What links these states is a concentration of graduate schools. Graduate students take out almost half of all federal loans issued each year, despite making up just 17% of enrolled students.23 Medical school, law school, and business programs are typically pricey for students.4

With an average student loan debt of $61,200, Mississippi stands out in the South. Though a significant number of its residents live in poverty (17.8%), its per-borrower average rivals Massachusetts, a state with double the per-capita income—and several graduate institutions.5 Demographics are part of the answer: Black borrowers carry disproportionately high balances nationally, owing an average of $25,000 more than white borrowers, and Mississippi has the highest Black population share of any state.6 The pattern is similar in South Carolina and Alabama.

Fast Fact

According to the Federal Reserve Bank of New York, the average total federal and private student loan balance per person is $54,600.1

Where Balances Are Falling—and Why

All but four jurisdictions (the 50 states plus Washington, D.C.) saw average per-borrower balances drop from 2024 to 2025.1 Wyoming fell the most, down $3,500 to $31,800, a 9.9% decline. North Dakota, Alaska, and Hawaii each dropped $2,900 or more.

Several factors are driving the decline. Biden-era forgiveness discharged almost $189 billion through the PSLF , income-driven repayment adjustments, and borrower defense claims—those covered by these often had the highest balances.3 And New York Fed data shows that, after pandemic-era forbearance ended in October 2023, a larger share of borrowers began reducing their balances, either through payments or loan forgiveness programs.7

The total for student loan debt nationwide still grew 2.5% year-over-year to $1.66 trillion in fourth quarter of 2025.8 But individual balances are moving in the right direction in most states, and where the average balances did increase—New Hampshire (+$1,100), Rhode Island (+$1,000), Illinois (+$300), and New Jersey (+$100)—the shifts were modest.

What OBBBA’s Repayment Overhaul Means for Borrowers

The One Big Beautiful Bill Act (OBBBA), signed in mid-2025, restructures federal borrowing starting on July 1, 2026. Graduate PLUS loans are going away for new borrowers. Parent PLUS loans will have a new $20,000-per-year cap and a $65,000 lifetime limit per student.9 All existing income-driven repayment plans (IBR, PAYE, SAVE) are being replaced for new borrowers with two options: a new standard plan and the Repayment Assistance Plan, which sets monthly payments at 1% to 10% of adjusted gross income, depending on earnings.10

Current borrowers can stay on existing plans until July 2028, when those enrolled in SAVE, PAYE, or ICR must switch.11

For states where high balances reflect graduate-school borrowing, such as Georgia, Maryland, Washington D.C., and Connecticut, the lower caps on Grad PLUS loans will likely lead to lower future debt loads. But they’re also likely to push many future law and medical students toward private loans that don’t have any federal protections, income-driven repayment plans, or any path to loan forgiveness.